A container lands. The supplier has invoiced correctly. The freight moved on time. Then customs clears the goods and the bill is far higher than the finance team expected.

That moment catches a lot of importers off guard, especially in the UK. Duty, import VAT, commodity codes, origin rules, and valuation all meet in one place. If even one input is wrong, the landed cost changes.

An import tax calculator helps you estimate that cost before the shipment moves, not after the goods are sitting at the port or airport. For UK importers, that matters more now because post-Brexit calculations follow UK-specific rules that many generic online tools do not explain well.

The Hidden Costs of Importing and Why You Need a Plan

A UK importer agrees a good unit price, books freight, and expects a healthy margin. Then the customs entry goes in, duty is added, import VAT is calculated on a wider value than the invoice alone, and the numbers no longer work.

That kind of surprise usually comes from a chain of small errors rather than one dramatic failure. A common pitfall is using the supplier’s product description as if it were a customs classification. Another is treating VAT as a percentage of the invoice price only, when customs often applies it to the taxable import value, which can include freight, insurance, duty, and other elements. Importers also assume a trade agreement rate applies, only to find they cannot support the claim with the right origin evidence.

Post-Brexit, UK importers also have a practical problem that many online guides gloss over. The rules are no longer an EU exercise with a different delivery address. The UK has its own tariff structure, its own customs procedures, and its own VAT treatment at import. If you use a calculator built mainly for US shipments, or a generic tool that skips UK-specific inputs, you can get an answer that looks tidy on screen and still fails in real life.

That matters long before the goods reach the port.

An accurate estimate affects your selling price, your cash-flow planning, the Incoterms you agree with the supplier, and whether the shipment makes commercial sense at all. It works a bit like checking the full cost of a mortgage rather than looking only at the headline monthly payment. The product price is only one part of the commitment.

Freightos makes the gap plain on its import duty calculator page, noting that its calculator “will soon be extended to include the UK”. For British importers, that gap is more than a content issue. It can lead to the wrong landed-cost assumptions at quoting stage, purchasing stage, and customs clearance stage.

Takeaway: An import tax calculator helps you plan the landed cost of a UK import so you can price correctly, protect margin, and avoid finding out too late that the shipment was never profitable.

What Is an Import Tax Calculator

A UK buyer agrees a price with an overseas supplier, books the freight, and then asks the question that should have been settled at the start. What will HMRC charge when the goods arrive?

An import tax calculator helps answer that question before the shipment reaches the border. It works like a mortgage calculator in one important sense. It gives you a grounded estimate based on the details entered, so you can judge affordability before you commit. For UK importers after Brexit, that matters because many online tools were built around US customs rules or generic assumptions that do not reflect UK tariff treatment, UK import VAT, or the evidence needed to support origin claims.

The key word is estimate.

A calculator does not replace classification work, origin checks, or broker review. It gives you a practical forecast of likely charges so you can budget landed cost, compare suppliers properly, and choose terms that suit your cash flow.

What you put into it

For a UK calculation to be useful, the inputs need to match how UK customs works in real life. At minimum, that usually means:

Commodity code

This is the tariff identity of the goods. In the UK, the duty rate depends on the 10-digit commodity code, not just a broad product description.Customs value

This is the value customs uses as the starting point for the calculation. In many cases, the transaction value is adjusted to include elements such as freight and insurance, depending on what is already included in the supplier’s price and the shipping terms. If you are unsure how those terms shift cost and risk, this guide to Incoterms 2020 for entrepreneurs is a useful reference.Country of origin

Origin is about where the goods are deemed to originate under customs rules, not the country they were shipped from. That distinction can change the duty rate completely, especially where a UK trade agreement may allow a reduced or zero rate.

What it gives back

A useful calculator usually returns two figures first:

- Estimated customs duty

- Estimated import VAT

Some tools also point out whether preferential origin may apply, whether anti-dumping or other trade measures could be relevant, or whether the goods may need extra paperwork.

Why UK-specific logic matters

For a British importer, a tidy number is not enough. The number has to reflect UK rules.

The official UK tariff tools are built around UK commodity codes and UK tariff treatment. A generic calculator, especially one designed mainly for US imports, can miss points that affect costs at clearance. Common gaps include UK import VAT treatment, the distinction between origin and shipping country, and the detail needed to classify goods at 10-digit level rather than using a broad HS heading.

That is where confusion often starts in practice. A calculator can look precise on screen while still being wrong for the shipment in front of you.

Where people get confused

A common misunderstanding is that the calculator creates the answer, when in fact, the user’s inputs do.

If the commodity code is wrong, the duty estimate will be wrong. If the customs value leaves out a cost that should be included, the VAT estimate will also shift. If a supplier says the goods are of UK agreement origin but cannot support that claim with the right evidence, the preferential rate may disappear at clearance or later review.

So the calculator is best treated as a decision tool. It helps you pressure-test the shipment before you buy, but the quality of the result depends on the quality of the information you feed into it.

The Core Components of an Import Tax Calculation

A UK import tax calculation works like a build sheet. You start with the customs value, apply the right tariff treatment to the right goods, and only then calculate VAT. If one part is wrong, the rest of the numbers shift with it.

Customs value comes first

Before duty rates mean anything, customs needs a value.

For UK imports, that usually means checking what the supplier’s price covers. A quote can include only the goods up to loading at origin, or it can include transport and insurance to the port. Those details matter because customs valuation depends on which costs sit inside the declared value and which still need to be added.

A simple comparison helps:

| Term | What it usually includes |

|---|---|

| FOB | Goods value up to loading at origin |

| CIF | Goods value plus cost, insurance, and freight to the port |

If the supplier quotes on something close to FOB terms, freight and insurance may still need to be added before duty is calculated. If the price is closer to CIF, fewer adjustments may be needed.

For a practical explanation of who pays for what under different shipping terms, see this guide to Incoterms 2020 international commercial terms.

Tip: Many bad estimates start with an invoice total that has never been checked against the shipping terms.

The commodity code decides the tariff treatment

In the UK, duty is linked to the 10-digit Commodity Code.

That level of detail matters more after Brexit because UK import entries must match UK tariff logic, not the assumptions built into broad international tools. A US-focused calculator may stop at a high-level HS heading. HMRC clearance does not. The code needs to match the exact product as imported.

That means looking at the goods the way customs does. What are they made of? What is their function? Are they complete items, parts, sets, or retail packs? Two products sold under the same commercial label can fall under different codes and attract different rates.

A calculator can only apply the right duty if the coding work is right first.

Origin affects whether the standard rate applies

After classification, the next question is origin for customs purposes.

This point catches many new importers because shipping country and origin are not the same thing. Goods can leave a warehouse in one country but still originate in another. For duty, origin is the legal test that decides whether a trade agreement rate is available.

The practical rule is straightforward. Preferential duty only applies if the goods meet the agreement’s origin rules and the importer can support that claim with valid evidence. Without that support, the standard UK rate may apply even if the supplier says the goods are covered by a trade deal.

That gap between commercial assumption and customs proof is one reason automated calculators can mislead. They can show a possible lower rate. They cannot confirm that your paperwork would survive an HMRC check.

A good visual explanation helps here:

Duty is calculated before import VAT

Once the customs value, commodity code, and origin position are settled, you can calculate duty.

For many goods, duty is ad valorem, which means a percentage of the customs value. Some products have more complicated tariff treatment, but percentage-based duty is the starting point for many UK commercial imports.

The sequence matters. Duty is usually worked out first. Import VAT is then charged on the taxable amount, which commonly includes the customs value and the duty. Many first-time importers miss that second step and budget only for the duty line.

That is how a shipment that looked affordable on the purchase order becomes more expensive at clearance.

Import VAT sits on top of the customs charge

For most UK business imports, import VAT is not calculated only on the goods price.

It is usually charged on the broader taxable base used at import, which often includes the customs value plus duty. In plain terms, VAT is applied after duty has increased the amount. That is why the VAT figure can feel higher than expected when someone has only looked at the supplier invoice.

A practical formula keeps the order clear:

Key formula: customs value → duty on that value → VAT on the duty-inclusive amount.

This is also where UK-specific calculation logic matters. Post-Brexit, businesses importing into Great Britain need a tool that reflects UK VAT treatment, UK coding, and UK tariff handling. A generic global calculator can look polished and still miss how the charges arise on a UK customs entry.

Cash flow matters as much as the tax rate

The rate tells you the size of the charge. The timing tells you how painful it will feel.

Import VAT can create a working-capital pinch if the business has to fund it before recovering it through normal VAT accounting. That is why many importers review whether Postponed VAT Accounting is available and appropriate for their setup. The tax may still be due. The accounting treatment changes how the cash impact lands.

For a growing importer, that difference can affect stock planning, pricing, and even whether a shipment should move this month or next.

What a reliable calculator must ask

A useful calculator should ask for the details that drive the result, not just a product description and an invoice figure.

At minimum, it should force you to confirm:

- What exactly are the goods? Enough detail to support the UK commodity code.

- What value basis are you using? Invoice value alone is often not enough.

- What is the goods’ origin for customs purposes? Origin must be established, not guessed.

- Could a preferential rate apply? Only if the rules are met and the proof exists.

- How will import VAT be accounted for? The answer affects cash flow, not just the headline tax.

If a calculator skips those questions and still produces a precise-looking answer, treat it as a rough estimate rather than a clearance-ready figure.

A Worked Example of a UK Import Calculation

A UK buyer agrees to pay £10,000 for a shipment of passenger vehicles from a country that does not benefit from a UK trade agreement. The invoice looks simple. The customs entry does not.

That gap catches importers after Brexit, especially if they have tested a calculator built around US import logic. A UK calculation usually does not stop at duty. Import VAT is calculated on a wider base, so the amount due at import can rise faster than a first estimate suggests.

Step 1, confirm the customs value

Start with the customs value. For this example, use £10,000.

Treat that figure as the foundation of the calculation. If the foundation is wrong, everything built on top of it is wrong too. In a live shipment, you would check whether freight, insurance, assists, or other additions should be included before customs accepts that value.

For a worked example, though, keeping the customs value at £10,000 lets you see the calculation clearly.

Step 2, apply customs duty

Assume the goods fall under a UK commodity code for passenger vehicles that carries 10% duty under the UK Global Tariff, with no preferential rate available.

The duty calculation is straightforward:

- Customs value: £10,000

- Duty rate: 10%

- Duty due: £1,000

This is often the point where a new importer thinks the hard part is over. It is not. Duty is only the first layer.

Step 3, calculate import VAT on the correct base

UK import VAT is charged on more than the goods value alone. It is usually calculated on the customs value plus duty, and in some cases other costs that belong in the VAT base.

In this simplified example, the VATable amount is:

- Customs value: £10,000

- Plus duty: £1,000

- VATable total: £11,000

If the VAT rate is 20%, the import VAT is £2,200.

A simple way to picture this is a stack. Customs starts with the goods value, adds duty on top, then applies VAT to the stack rather than to the bottom layer on its own.

Step 4, add the charges together

The import taxes due are:

- Duty: £1,000

- Import VAT: £2,200

- Total import taxes: £3,200

So a shipment purchased for £10,000 can create £3,200 in import taxes before inland haulage, port charges, storage, brokerage, or delivery are added.

Why this example matters practically

Here, theory turns into operational decisions.

If one supplier offers a lower unit price but the goods do not qualify for preference, that cheaper quote may produce a worse landed cost than a higher-priced supplier whose goods meet the origin rules. If the shipment is time-sensitive, the way those charges fall can also affect whether you import now, split the consignment, or review the Incoterms with the seller.

That is why UK-specific calculations matter so much post-Brexit. A generic online calculator can look polished and still miss how a UK customs entry is built in practice.

If your supply chain includes Asian sourcing, transport costs and tax need to be reviewed together. This guide to shipping China to the UK is useful for that wider landed-cost planning.

Key lesson

The arithmetic is the easy part. The commercial risk sits in the inputs.

A calculator can only produce a reliable answer if the commodity code is correct, the customs value is built on the right basis, and any origin claim can be supported with evidence. That is the difference between an estimate that looks tidy on screen and a figure your customs agent can safely declare.

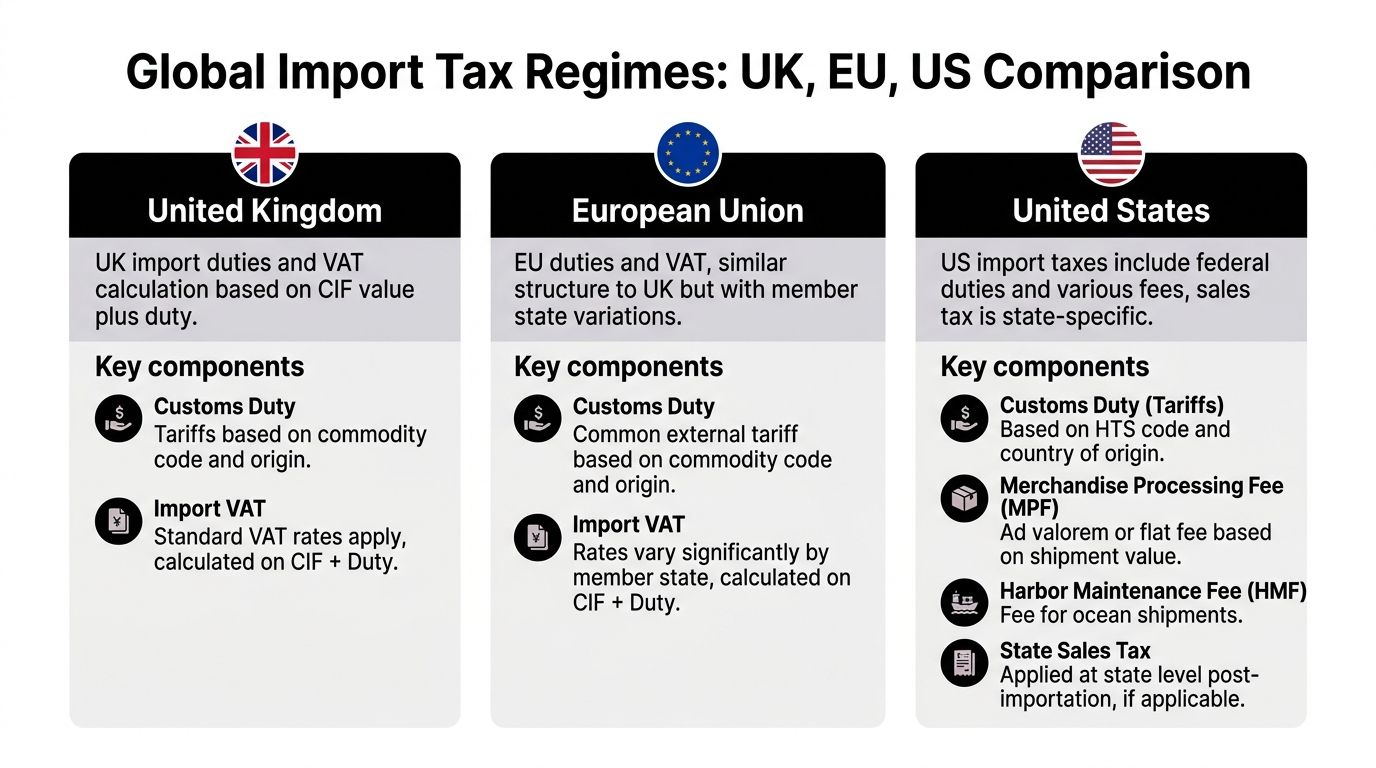

Navigating Global Differences in Import Taxes

A UK buyer can compare two online calculators, enter the same shipment details, and get two very different answers. One tool is built around US entry fees and tariff logic. The other reflects how UK customs entries are assessed. If you rely on the wrong model, your margin can disappear before the goods leave the port.

Why the comparison matters

Import tax rules are not interchangeable.

A US importer often starts with customs duty and specific entry fees. A UK importer usually has to account for customs duty and import VAT, with VAT calculated on a wider base than many first-time importers expect. An EU importer may also face duty and import VAT, but the VAT rate and the local filing process depend on the member state where the goods are cleared.

That difference affects more than the customs entry. It changes landed cost, selling price, cash flow, and even where a business chooses to import the goods in the first place.

A simple side-by-side view

| Region | Main tariff system | Main import tax treatment | Practical issue |

|---|---|---|---|

| United Kingdom | UK Global Tariff | Duty plus import VAT | UK commodity code, customs value, and origin must all align |

| European Union | Common external tariff | Duty plus import VAT | VAT rates and import procedures vary by member state |

| United States | HTS-based duties and fees | No national import VAT equivalent in the UK or EU sense | Sales tax sits outside the customs calculation in a different way |

For a UK business, that last row matters a great deal. Many online tools are written from a US perspective, so they estimate duty well enough but do not model the full UK tax position with the right emphasis on import VAT.

The UK now needs its own lens

Post-Brexit, the UK is no longer a variation of an EU import example. It is its own customs environment, with its own tariff, its own treatment of trade agreement claims, and its own practical filing habits.

That catches businesses out.

A calculator may look polished and still guide the user toward the wrong assumptions if it was designed around US terminology or older EU workflows. Terms such as HTS, broker fee, or sales tax can sound familiar enough to reassure the user, but they do not tell you how a UK declaration is built or how HMRC will view the entry.

The safest starting point is simple. Use a tool and a method that match the country where the goods are being imported.

Where online tools usually fall short

The weak spots tend to be predictable:

Import VAT is simplified too much

Some calculators highlight duty and hide the VAT effect, even though VAT is often the larger figure in a UK entry.Preference is treated as automatic

A tool may display a lower duty rate because a trade agreement exists. That does not mean the goods qualify, or that the importer holds the evidence needed to support the claim.Terminology does not match UK practice

US-focused tools often describe the process in a way that does not map cleanly to UK customs work, which makes errors more likely during quoting and budgeting.Multi-country supply chains are flattened into one answer

Goods may be manufactured in one country, shipped from another, and imported into a third. A generic calculator can miss how that affects origin, valuation, and the final tax result.

A practical comparison helps here. Using a US-based calculator for a UK import is a bit like using miles to price a journey that will be billed in kilometres. The arithmetic can still look neat, but the commercial answer is off.

The decision point for multi-market importers

If you import into the UK and then sell into the EU or the US, you need a separate landed-cost model for each destination. One shared calculator is rarely enough.

That is how experienced importers avoid three expensive mistakes. They do not quote customers on the wrong tax basis. They do not choose an Incoterm that pushes unexpected liability onto the wrong party. They do not route stock through the wrong country because an online estimate made the option look cheaper than it really was.

The rule is straightforward. Match the calculator to the country of import, then sense-check the result against the customs position before you build prices or commit to a shipping plan.

Common Pitfalls and Limitations of Automated Calculators

Automated tools are useful. They are not self-checking, and they do not replace customs judgement.

That matters because a calculator can only process the information you feed it. It cannot tell you that your product description is too vague, your supplier’s origin statement is weak, or your invoice structure creates a valuation problem.

Wrong commodity code, wrong result

The biggest practical limitation is classification.

In the UK, import duty is determined by the 10-digit Commodity Code and country of origin. HMRC-linked guidance notes that misclassification and undervaluation remain common, and 2025 Q1 HMRC stats revealed 18% of EU-UK LCL shipments underdeclared value to skirt 20% VAT, risking penalties up to 100% of the evaded duty, according to the UK Trade Tariff guidance.

A calculator cannot correct a bad code choice unless the user already suspects the code is wrong.

Origin is often assumed, not proven

Many users click the lower duty option because a trade agreement exists. That is where trouble starts.

A calculator may show the potential preferential rate, but customs still expects the goods to satisfy the agreement’s origin rules and for the importer to hold suitable evidence. Without that, the lower rate may not be available.

Valuation errors are quiet but expensive

Another weak point is customs value.

Teams often enter the supplier invoice value without checking whether freight, insurance, commissions, assists, or other relevant elements affect the customs value. The calculator then returns a neat answer built on a faulty base.

Because the maths looks tidy, people trust it too quickly.

Broker’s view: The dangerous errors are not the obvious ones. They are the entries that look reasonable enough to pass internal review, then fail in a customs audit.

Calculators do not capture every barrier

Import taxes are not the only thing that can affect release or total cost.

Depending on the goods, importers may also need:

- licences

- quota checks

- regulatory approvals

- product marking compliance

- inspection-related documents

An automated tax estimate may still be arithmetically correct while being operationally incomplete.

Human review still matters

Use calculators for speed and planning. Then apply human review where the commercial exposure is meaningful.

That is especially true when:

- the goods are hard to classify

- origin is mixed or processed in several countries

- the shipment value is commercially significant

- the product is regulated

- your margin is tight enough that a tariff mistake changes the viability of the sale

A reliable process is not calculator versus expert. It is calculator first, expert verification where the risk justifies it.

Achieve Certainty with Multica Group’s Customs Expertise

Importing gets easier when the estimate is no longer the final goal. The ultimate goal is confidence that the code, value, origin, and documents will stand up when customs reviews the entry.

That is where a logistics partner with in-house customs capability becomes useful. Multica Group supports businesses moving goods across Europe, Asia and the United States with freight forwarding, customs clearance, documentation support, warehousing, and regulated shipment handling.

For importers, that matters in practical ways. A team can review classification before the goods depart, sense-check whether origin evidence supports a preferential claim, and spot where the chosen Incoterm may create valuation or responsibility issues.

That support is particularly valuable for regulated or time-sensitive cargo. If the shipment also involves veterinary inspections, life sciences requirements, or tight delivery windows, customs work cannot sit in a silo. It has to connect with the freight plan itself.

Multica’s broader service offer is outlined in its page on international freight forwarding services. The key point is not transport capacity alone. It is the combination of transport, customs handling, and documentation control in one workflow.

If your business is still relying on generic calculators and supplier assumptions, that is usually the point where hidden cost becomes avoidable cost. Expert review will not remove duty or VAT, but it can reduce the risk of paying the wrong amount, delaying the release, or building pricing decisions on shaky numbers.

Frequently Asked Questions About Import Taxes

Do import taxes apply only to commercial shipments

No. Import taxes can also apply to non-commercial goods, although the treatment can differ depending on the shipment type, value, and reliefs available. The key point is that customs looks at the facts of the import, not just whether the consignee is a business.

How often do duty rates change

Duty rates do not usually change every week, but they can change when tariff policy, trade agreements, or customs rules are updated. That is why importers should check the current tariff position before shipping, especially when they are pricing goods months in advance.

What is a de minimis threshold

A de minimis threshold is a value below which certain import charges may not apply, or may apply differently. In UK practice, thresholds can affect low-value consignments, but importers should be careful not to treat them as a shortcut. The shipment facts, the goods, and the transaction structure still matter.

Can I rely entirely on my supplier’s product description

No. Supplier descriptions are often written for sales or packing purposes, not for customs classification. A phrase like “accessories” or “components” is rarely enough to support a reliable commodity code.

Is a lower duty rate always available if a trade agreement exists

No. A trade agreement may create the possibility of a lower rate, but the goods must satisfy the agreement’s rules of origin and the importer must hold suitable evidence. Without that, customs may apply the standard rate instead.

What is the biggest mistake first-time importers make

Most first-time importers focus on the duty percentage and ignore valuation, VAT treatment, and documentation. The full customs cost comes from the full calculation, not one line of it.

If you want a clearer landed cost picture before your next shipment moves, Multica Group can help you connect freight planning with customs reality. That means fewer assumptions, cleaner documentation, and more confidence in what your goods will cost to import into the UK.