A lot of shippers only find out what their cover really means when something has already gone wrong.

The pattern is familiar. A pallet of chilled food sits too long after a border inspection. A carton of electronics arrives with water damage after an ocean leg. A pharma shipment reaches the consignee, but the packaging shows a temperature excursion and the goods can’t be released. The carrier accepts the incident report, then offers compensation that has very little to do with the commercial value of what was lost.

That’s where confusion starts. Many businesses think transport risk is handled because the carrier is involved, the freight documents are in order, and someone somewhere has “insurance”. In practice, those are three separate issues. Carrier liability, cargo insurance, and operational risk control each solve a different problem.

Insurance for cargo works best when you treat it as part of shipment design, not an afterthought. Its purpose is to protect margin, cash flow, customer commitments, and stock availability across road, sea, and air movements between Europe, Asia, and the US. That matters even more on post-Brexit EU-UK lanes, where customs formalities, inspection delays, handovers, and multimodal transfers create more opportunities for a small problem to become an expensive one.

Your Cargo Is At Risk But It Does Not Have To Be

A shipment can move perfectly for most of its journey and still arrive as a financial problem.

Take a straightforward example. You import high-value goods from Asia in a sealed container. The vessel encounters heavy weather, moisture gets into the load, and the goods arrive visibly damaged. From an operations standpoint, the movement is complete. From a finance standpoint, it has just begun. The buyer still has disrupted stock, the seller still has a commercial dispute, and the carrier may only respond within its legal liability limit.

That gap is why insurance for cargo matters. It isn’t paperwork for its own sake. It’s the mechanism that turns an unpredictable transport loss into a manageable commercial event. In the UK, this sits inside a mature marine insurance market with deep global influence. Europe, led by the UK, accounted for 37.68% of global cargo insurance premiums in 2024, and the market’s legal foundation still reflects the principles of the Marine Insurance Act 1906, according to the IUMI market update on cargo insurance in 2024. The same source notes that cargo insurance helps mitigate over 70% of multimodal transport risks.

Practical rule: If losing one shipment would damage your cash flow, customer relationship, or regulatory position, you need more than a carrier’s default liability.

The aim isn’t to insure everything in the same way. It’s to match protection to the goods, route, handover points, and likely failure modes. That matters most when you’re moving regulated, fragile, perishable, or high-value cargo across several jurisdictions.

Why Carrier Liability Is Not Cargo Insurance

The most expensive misunderstanding in shipping is simple. Many cargo owners assume the carrier’s responsibility means the cargo’s full value is protected.

It isn’t.

Carrier liability is a legal framework. Cargo insurance is first-party financial protection bought for the cargo owner’s interest. Those are not interchangeable. One standardises what a carrier may owe in certain situations. The other is designed to protect the value of the goods themselves.

The liability gap is where losses become painful

For UK road haulage, the problem is often hidden until claim time. Under RHA standards, standard carrier liability can leave major underinsurance gaps, and 40% of claims pay only a fraction of the actual loss. For international road freight, the CMR Convention liability cap is 8.33 SDR per kilogram, roughly £7/kg, which is often nowhere near enough for high-value goods. The same source notes an 18% rise in unresolved road cargo claims post-Brexit. That’s set out in this analysis of freight cargo insurance and liability limits.

If you ship heavy, low-value goods, that limit may still feel inadequate, but survivable. If you ship light, high-value goods, it can be commercially absurd. A carton of medical devices, electronics, specialist ingredients, or temperature-sensitive pharmaceuticals can hold a value that bears almost no relation to its weight.

A simple way to think about it

Carrier liability is like relying on the other party’s minimum legal obligation after a road accident. Sometimes it helps. Often it doesn’t restore your position.

Cargo insurance is the policy you arrange so you’re not dependent on arguing over fault, convention limits, packaging allegations, or handling disputes while your stock is missing and your customer is waiting.

The question isn’t whether the carrier is responsible. The question is whether the recovery matches the loss you actually suffer.

What works and what doesn’t

A few practical distinctions matter here.

- What works for low-risk, low-value movements: If the goods are easy to replace, time pressure is limited, and the financial exposure is modest, some shippers accept the liability gap.

- What fails for regulated or valuable cargo: Pharma, electronics, specialist machinery parts, branded retail stock, and agri-food products usually can’t absorb that gap without pain.

- What often gets missed in multimodal chains: Liability changes as the mode changes. A movement that starts by road, transfers to sea, then finishes by road can involve several legal regimes and several opportunities for argument.

Why post-Brexit movements need more discipline

EU-UK traffic now creates more handovers, more formalities, and more chances for delay. Every additional stop, customs event, warehouse handling point, or border process increases the number of moments where loss, theft, temperature drift, or documentary mismatch can occur.

That matters because carrier liability is reactive and narrow. It doesn’t protect your gross margin, your customer SLA, your replacement cost, or the knock-on cost of a failed launch, rejected delivery, or regulatory hold.

A shipper who treats liability as insurance usually learns the difference at the worst possible moment. A shipper who buys insurance for cargo based on the actual value and risk profile of the goods gives the finance team, the operations team, and the customer a much stronger outcome.

Decoding the Main Cargo Insurance Policy Types

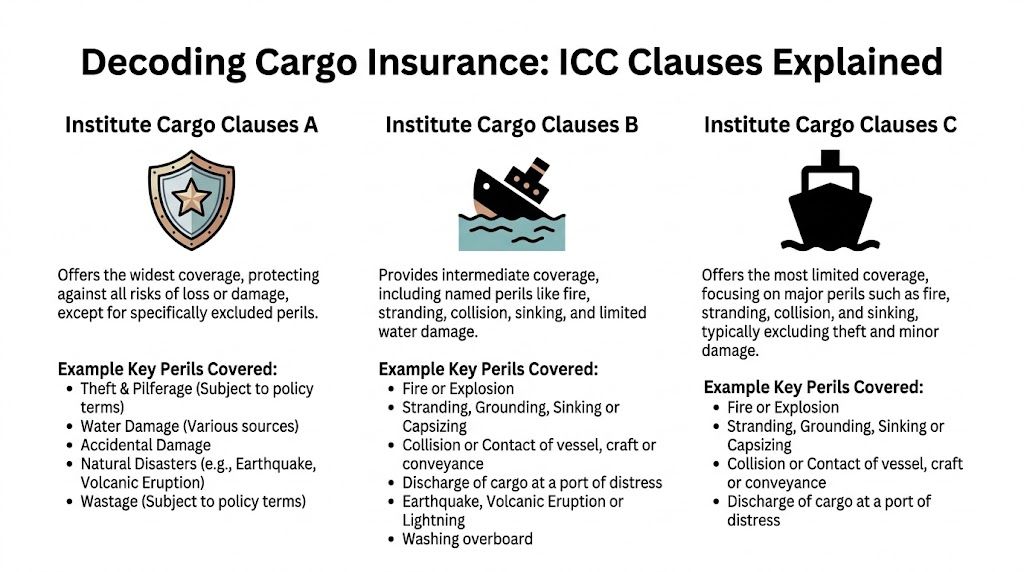

Once you ask for cover, you’ll usually run into the Institute Cargo Clauses, often shortened to ICC. These clauses are the backbone of many marine cargo policies and, by extension, of many multimodal insurance arrangements that include an ocean leg.

The practical decision usually comes down to ICC (A), ICC (B), or ICC (C). The letters look harmless. The difference in outcome can be substantial.

Think of these clauses like levels of cover

The easiest analogy is motor insurance.

ICC (C) is the most limited. It’s the closest thing to catastrophe-only thinking. It usually responds to major named events such as fire, collision, stranding, or sinking.

ICC (B) adds more named perils. It sits in the middle. It gives broader protection than ICC (C), but it still depends on the event fitting a listed cause.

ICC (A) is the broadest standard option and is commonly described as all risks cover for physical loss or damage, subject to exclusions. That phrase matters. It does not mean absolutely everything is covered. It means the policy starts from a wider grant of cover, then carves out exclusions such as inherent vice or insufficient packing.

Why ICC A usually makes commercial sense

For many shippers, the core value of ICC (A) is not only breadth. It is clarity.

When you buy named perils cover, the claim can become an argument about whether the exact cause fits the wording. Was the damage due to sea water, condensation, rough handling, poor stowage, or packaging weakness? Was there a major insured peril, or only a partial loss event? The narrower the wording, the more room there is for dispute.

For UK trade lanes, that difference shows up in recoveries. UK P&I Club data indicates 25-30% higher claim recovery rates for ICC(A) all-risk policies on EU-UK routes. For high-value goods, premiums for ICC(A) with a 110% insured sum average 0.3-0.8% of cargo value, according to the Berkley Offshore marine cargo FAQ.

Client advice: For cargo that is valuable, regulated, fragile, branded, temperature-sensitive, or difficult to replace, start by asking why you would accept narrower cover, not why you’d buy broader cover.

Comparison of Institute Cargo Clauses ICC

| Peril / Event | ICC (C) – Basic | ICC (B) – Standard | ICC (A) – All Risks |

|---|---|---|---|

| Fire or explosion | Typically covered | Typically covered | Typically covered unless excluded |

| Vessel stranding, sinking, collision | Typically covered | Typically covered | Typically covered unless excluded |

| Water damage | Limited | Broader than ICC (C) for named situations | Generally covered as external physical loss or damage unless excluded |

| Theft | Commonly not the right fit unless specifically addressed | May be limited | More suitable than named perils cover, subject to policy wording |

| Rough handling in transit | Often difficult to recover under narrow wording | Depends on whether the event matches a named peril | More likely to fit, unless an exclusion applies |

| Partial damage not caused by a major casualty | Often problematic | Can still be restrictive | Better suited to these losses |

| Poor packaging | Excluded | Excluded | Excluded |

| Inherent vice or natural deterioration | Excluded | Excluded | Excluded |

| Delay alone | Excluded | Excluded | Excluded |

What each clause means in the real world

ICC C suits very narrow risk tolerance

ICC (C) can work where the goods are durable, low value, and not especially vulnerable to handling, moisture, pilferage, or partial damage. Think of it as protection against severe transport casualties, not everyday transit problems.

If your exposure is mainly catastrophic loss and you can absorb lesser damage, it may be acceptable. Most businesses moving sensitive stock across multiple handovers can’t rely on it comfortably.

ICC B is a halfway house

ICC (B) gives broader named perils cover and can fit some mid-risk cargo. The challenge is that many costly shipment problems don’t arrive with a clean, obvious cause. They arrive as damaged cartons, wet packaging, shifted pallets, contaminated product, or compromised seals.

That’s where named perils can disappoint. You may still have a genuine loss and a weak recovery.

ICC A is the working standard for serious shippers

For pharma, electronics, branded retail, specialist components, and much of agri-food logistics, ICC (A) is usually the sensible starting point. The premium is a visible cost. The wider protection is often far cheaper than one disputed claim.

It’s also common to insure at 110% of cargo value so the policy reflects not just invoice value but associated commercial exposure. That doesn’t solve every problem, but it recognises that a shipment loss usually costs more than the goods alone.

The mistake isn’t buying insurance for cargo. The mistake is buying a level of cover that looks acceptable in a quote summary but fails under ordinary transit conditions.

How Incoterms Define Your Insurance Responsibility

Insurance responsibility often becomes muddled long before the goods move. The issue starts in the sales contract.

Incoterms decide where risk transfers from seller to buyer. If you don’t align insurance with that handover point, one leg of the journey may be uninsured, or both sides may end up paying for overlapping cover without realising it.

The handover point matters more than the label

A lot of disputes come from people recognising the three-letter term but not understanding the exact risk transfer point.

With EXW, the buyer takes responsibility very early, effectively from collection at the seller’s premises. If you buy under EXW and assume the seller’s policy protects the movement out of origin, you may already have a gap.

With FOB, the key handover is when the goods are loaded on board the vessel. Many importers focus on the ocean leg but forget what happens before loading and after discharge.

With CIF, the seller must arrange insurance to the destination port. That sounds reassuring, but buyers still need to check the quality and scope of that cover. “Insurance provided” and “adequate insurance for my risk profile” are not the same thing.

With DDP, the seller carries responsibility much further, often to the named destination. That can simplify the buyer’s position, but only if the operational execution and documentation are sound.

For a deeper operational explanation of risk transfer points, this guide to Incoterms 2020 for international trade is useful.

Four terms that regularly cause confusion

EXW

Best for buyers who want maximum control and are ready to manage collection, export formalities, main carriage, and insurance from the start.FOB

Common in ocean freight. Useful, but easy to misunderstand if the team doesn’t map the pre-loading and post-arrival legs.CIF

Often treated as “the seller has sorted insurance”. Sometimes they have. The better question is what standard of cover they bought, for whose benefit, and whether it fits the actual cargo.DDP

Commercially attractive for buyers who want a delivered solution. Risk sits with the seller for longer, but claims can still become messy if the delivery chain is subcontracted and highly fragmented.

A short visual overview helps if your sales and logistics teams need to align on terms before booking transport.

Where shippers get caught out

The common failure is not legal complexity. It’s operational laziness.

A buyer assumes the seller’s insurance runs warehouse to warehouse. The seller assumes the buyer’s open cover starts earlier than it does. The forwarder books according to shipping instructions that don’t reflect the sales contract. Then a loss occurs during a transfer, storage period, customs hold, or first-mile collection, and everyone discovers that the “insured leg” wasn’t the damaged one.

Check the contract, the booking, and the insurance certificate together. If those three don’t line up, the shipment has a built-in weak spot.

Navigating Premiums Exclusions and Claims

A cargo policy should never be judged only by the premium line. Price matters, but wording, exclusions, declarations, and claims handling discipline matter more when something goes wrong.

Premiums have softened for some standard transit risks. The global cargo insurance market saw premium adjustments of -4% to -7.5% in 2024 for standard transit cargo because insurer capacity increased, according to Grand View Research’s logistics insurance market analysis. That doesn’t mean every shipper gets cheaper cover. High-risk profiles still price differently, particularly where theft exposure or cargo sensitivity is high. The same source highlights average cargo theft values of $281,757 per incident in Q1 2024.

What drives the premium

Underwriters usually look at the same core variables, but they don’t weigh them equally for every shipment.

Cargo type changes everything

A pallet of metal fittings and a pallet of biotech product don’t belong in the same insurance conversation. Fragility, resale value, theft appeal, spoilage risk, contamination risk, and regulatory sensitivity all affect how an insurer views the shipment.

High-value, lightweight cargo often costs more to insure because the potential loss is large relative to the physical shipment size. Perishables can also attract tighter scrutiny because a short delay or a refrigeration failure can render the goods commercially worthless even when the packaging looks intact.

Route and mode shape the exposure

Sea freight introduces weather, moisture, stowage, and port handling risks. Road freight introduces theft, collision, and unsecured stop risks. Air freight can reduce transit time but creates its own documentation and handling sensitivities.

Multimodal chains matter most because each transfer point increases the chance of loss, delay, or miscommunication. A policy that looks broad can still become awkward if the shipment includes storage, cross-docking, customs holds, or final-mile distribution that wasn’t clearly contemplated.

Sum insured and declarations affect recovery

If the insured value is wrong, the claim can become harder than it needed to be. Declaring the cargo inaccurately, understating value, or failing to align the policy with invoices and transport documents creates avoidable friction.

That’s especially dangerous for repeat shippers using open cover or annual arrangements. A good policy can still produce a poor result if declarations are weak.

Exclusions are where confidence gets tested

Even broad all-risk cover has exclusions. In practice, the most important ones are often the least glamorous.

- Insufficient packaging: If the goods were not packed for the actual conditions of road, sea, or air transit, insurers may resist the claim.

- Inherent vice: If the product naturally deteriorates or is unstable by its own nature, that’s often outside standard cover.

- Delay on its own: Delay can trigger major commercial loss, but delay by itself is commonly not an insured peril.

- War, strikes, and related risks: These are often handled separately or added by endorsement.

- Known or preventable issues: If the shipment was sent with obvious defects, poor declarations, or unmanaged temperature requirements, the claim may face challenge.

A policy doesn’t rescue poor shipment preparation. Insurance responds to insured transit risks. It doesn’t repair a weak process.

Claims that get paid usually follow a disciplined pattern

When loss or damage is discovered, speed and evidence matter.

- Notify immediately. Tell the insurer or broker as soon as the issue is identified.

- Protect the cargo. Prevent further damage where possible without destroying evidence.

- Document what you see. Photos, seal condition, packaging state, pallet positions, temperature records, and delivery exceptions all matter.

- Hold the carrier on notice. Preserve recovery rights even if you expect to claim under your own policy.

- Keep the paper trail clean. Commercial invoice, packing list, transport documents, survey reports, and correspondence should all line up.

A claims file is easier to defend when operations, warehouse staff, and the consignee all report the same facts. Most claim problems aren’t caused by one missing document. They come from inconsistent evidence, late notification, and assumptions that someone else has logged the issue properly.

Proactive Risk Management for Shippers

Good insurance is a backstop. Good operations are the first defence.

Most avoidable cargo losses start before the vehicle moves. They begin with weak packaging, poor instructions, incomplete data, unsuitable handover planning, or a shipment profile that was treated as routine when it wasn’t.

Packaging is not a warehouse detail

Packaging has to match the transport environment, not the ideal one. A carton that survives domestic parcel movement may fail badly in a multimodal chain involving palletisation, port handling, consolidation, deconsolidation, and wet conditions.

For dense or fragile goods, that means thinking about compression strength, internal bracing, moisture resistance, and load stability. For export timber packaging, it means making sure compliance and structural fitness are both addressed. If you need a practical reference point, this guide to crating for shipping is a useful reminder that packaging is part of risk control, not just presentation.

Perishables and pharma need tailored controls

Perishable and regulated goods are where standard assumptions fail fastest. A 2024 UK Freight Transport Association survey found 41% of agri-food exporters lacked specialized insurance for refrigeration failure or inspection delays, and 35% of cases resulted in denied claims because standard policies often exclude those scenarios, according to this overview of cargo coverage gaps for perishable goods.

That finding matches what operators see in practice. A chilled load can be commercially lost without visible impact to the pallet. A pharma shipment can become unsellable because the temperature record, inspection timing, or product integrity trail is no longer acceptable.

Three controls that prevent expensive surprises

Tight documentation

Border delays, customs queries, and inspection holds often start with small documentary errors. Commodity descriptions, values, origin data, health paperwork, and handling instructions all need to be consistent across the document set.

For regulated goods, documentation is not an admin task delegated at the last minute. It is part of product protection.

Live visibility

GPS tracking, telematics, temperature loggers, and event alerts don’t replace insurance, but they reduce uncertainty fast. They help the team intervene early, reroute if needed, and produce evidence if a claim follows.

For theft-sensitive goods, visibility also changes behaviour. Secure routing, fewer unscheduled stops, and cleaner handover records reduce the practical chance of a loss.

Carrier and route discipline

The cheapest route is often the least controlled route. If the goods are high consequence, use service patterns that minimise unnecessary handling, idle time, and handovers.

This is especially important on post-Brexit lanes where veterinary checks, customs processes, and cross-docking can expose cargo to temperature drift, delay, and security risk.

The strongest cargo programmes treat insurance, packaging, documentation, and tracking as one system. If one part is weak, the others work harder and still may not save the shipment.

How Multica Group Simplifies Your Cargo Insurance

Cargo insurance gets easier when the transport plan is organised properly from the start.

That’s where an experienced freight partner adds value, even without acting as the insurer. A team that understands road, sea, and air movements across Europe, Asia, and the US can spot the practical weak points early. That includes handover risks, customs exposure, temperature-sensitive legs, documentation mismatches, and the places where Incoterms and operational reality don’t line up.

Multica Group supports that process through its multimodal freight expertise, customs handling, documentation support, and visibility across complex shipments. If you’re coordinating road freight, ocean freight, air movements, warehousing, or cross-docking, their freight forwarding services help reduce the operational mistakes that often sit behind cargo losses and disputed claims.

The point isn’t only to move the goods. It’s to move them in a way that makes the insurance arrangement more effective. Better planning, cleaner paperwork, more controlled handling, and stronger visibility all make a claim less likely and a recovery more straightforward if one is needed.

That matters most when the cargo is regulated, perishable, high value, or commercially time-critical. In those cases, insurance for cargo works best alongside a logistics set-up that is built to avoid preventable loss in the first place.

Frequently Asked Questions About Cargo Insurance

Do I need cargo insurance if the carrier already has cover

Usually, yes. The carrier’s cover protects the carrier’s liability position, not necessarily the full value of your goods. If the legal liability cap is lower than the cargo value, or if the carrier disputes responsibility, your recovery may fall well short of the actual loss.

Is all-risk cover the same as cover for everything

No. All-risk usually means broad protection for physical loss or damage unless the policy excludes the cause. It does not mean every commercial problem is insured. Delay, poor packaging, inherent vice, and some special risks are common pressure points.

Should I insure only the invoice value

That’s often too narrow. Many shippers insure on a basis that reflects the cargo value plus an additional margin recognised by the policy wording. The aim is to account for the wider commercial exposure tied to a shipment loss, not just the cost of the goods on paper.

What is warehouse-to-warehouse cover

It generally means the insurance can extend beyond the main transport leg and respond from the point goods leave origin through to final destination, subject to the wording and any storage limits or conditions. It’s especially useful when the movement includes collection, port handling, temporary storage, customs events, and final delivery.

Does cargo insurance cover spoilage

Not automatically. For agri-food, chilled products, frozen loads, and many pharma movements, spoilage, refrigeration breakdown, and temperature excursion often need specific attention in the policy wording. If your goods depend on a controlled environment, ask direct questions and get the answer in writing.

What is general average and why should I care

General average is a long-standing maritime principle under which cargo interests can be asked to contribute to extraordinary costs incurred to preserve the voyage in a common emergency. Even if your own cargo is not physically damaged, you may still face a contribution demand. Many shippers don’t think about it until their goods are effectively held pending security.

What should my team do first if cargo arrives damaged

Start with evidence and notification.

- Record the condition immediately: Take photographs before unpacking further where possible.

- Note exceptions on delivery documents: If the packaging, seal, or pallet condition is wrong, write it down at receipt.

- Notify the insurer or broker quickly: Delay weakens claims.

- Retain all supporting paperwork: Invoice, packing list, transport documents, temperature logs, and correspondence should stay together.

- Don’t dispose of damaged goods too early: Surveyors or insurers may need to inspect them.

Is open cover better than insuring shipment by shipment

For frequent shippers, open cover is often more practical because it standardises terms and reduces the risk of forgetting to insure a movement. For occasional shipments, single-shipment cover may be enough. The right answer depends on shipment frequency, cargo profile, route complexity, and how disciplined your declarations are.

If your business moves goods across Europe, Asia, or the US, Multica Group can help you reduce the operational risks that make cargo claims expensive in the first place. From multimodal freight and customs support to documentation control, warehousing, and time-critical transport, Multica helps importers and exporters build a more resilient shipping process around the realities of insurance for cargo.